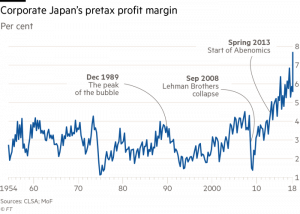

Japan’s stock market hasn’t done much this year – the Nikkei is up about 4% YTD – but you can’t blame that on poor corporate earnings growth. Earnings for the Nikkei are up about 30% year over year and profit margins are hitting new highs (from the FT):

Shinzo Abe introduced his three arrows reform plan when he was elected in 2012. The three arrows were fiscal stimulus, monetary easing and structural reforms. Most analysts have concentrated on the first two of those but I have said consistently since we made our first investments in Japan – just before Abe was elected by the way – that the structural reforms were the most important.

These structural reforms have prodded companies to concentrate more on measures of efficiency rather than just pursuing revenue growth. Companies have been encouraged to raise returns on equity, diversify their boards of directors, unwind cross shareholdings, hire more women and generally be more shareholder friendly. Structural reforms also include liberalizing the agriculture and electricity sectors, cutting the corporate tax rate (although it is still too high), creating special economic zones and liberalizing immigration.

All of these reforms have been successful to one degree or another but the change in corporate performance is the most stark. It is nothing less than a revolution and Japan is the only major developed economy pursuing such big changes.

There are a lot of misconceptions about Japan. Investors seem to believe that nothing has changed there over the last thirty years but that just isn’t true. And their economic performance was never as bad as the perception anyway. On a per capita basis, Japan’s economic growth has been quite competitive. Indeed, in the last decade Japan’s growth per capita has equaled the US and has been better than most of Europe.

The big problem for Japan has been and continues to be demographic. With a shrinking population the only path to growth has been improvements in productivity. The problem may not be as dire as some think though. Japan leads the world in robotics and they are raising the retirement age.

Investment managers around the world are still underweight Japan equities but if their recent economic and corporate performance continues that won’t last. From my perspective it is hard to justify buying US stocks at over 20 times earnings when I can buy Japan at 12 times, especially with earnings growth every bit as good as the US – and improving.

Sources:

Japan’s Successful Economic Model – Adair Turner – Project Syndicate

Japan’s Corporate Performance Highlights Bull Case – Leo Lewis – FT

Profits Jump at Japanese Companies but Foreign Investors Don’t Bite – Mike Bird – WSJ

The Third Arrow Of Abenomics: A Scorecard – Robin Harding – FT

{kind=link}