{kind=link}

Among America’s older population there is a growing concern about the state of their retirement and many are choosing to stay in the workforce much longer. In a previous article I listed concerns of older workers about whether they will ever be able to retire; concerns that include whether they’ve saved enough money, the amount they lost during the Great Recession, the housing crash, the constantly upward spiral of healthcare costs and the need for medical insurance, and the fact that people are living longer.

Of particular concern is the viability of Social Security. Will it be there? How much will I receive? Unfortunately, an American myth has developed over almost 9 decades that Social Security will provide most or all the money for wonderful, carefree golden years. But Social Security was always supposed to be a supplement. It was never intended as a person’s sole retirement income.

For years there’s been the discussion about a failing Social Security system that will run out of money. Politicians have used it as a campaign issue but Congress keeps kicking the can down the road giving it nothing more than lip service. For the first time, in 2017, the Federal Government sent more money to retirees and disabled workers than it collected in payroll taxes. Problems with Social Security are no longer theories. They’re a reality. And it’s no wonder older Americans are continuing to work.

To their credit, the trustees of the Social Security trust fund have been warning everyone that the piper would have to be paid. For more than 20 years, every individual’s annual Social Security statement has contained a notice similar to this one from 2001:

By 2038, the trust funds will be exhausted and the payroll taxes collected will be enough to pay only about 73 percent of benefits owed.

If you look at your most recent statement, you’ll find a statement just like it.

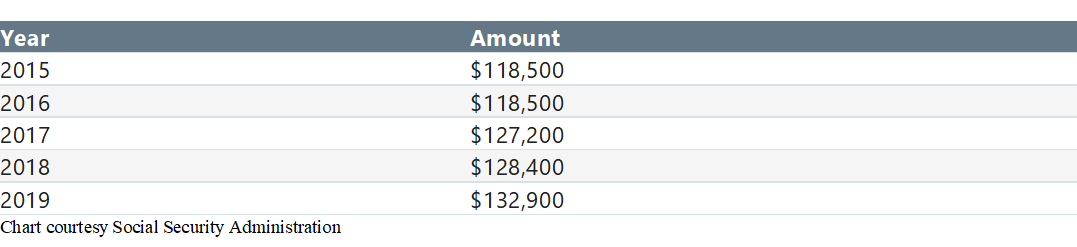

The Social Security system has tried to stem the tide of a potential future underfunding by raising the maximum amount of income taxable for Social Security from $3,000 at the beginning of Social Security to $132,900 in 2019.

Maximum Taxable Earnings Each Year

The theory of having a solvent Social Security system has always been growth—more generations, more babies, and eventually more workers paying into the system. The theory isn’t working.

At the inception of Social Security in 1935, there were substantially more workers contributing to the system than the number receiving benefits. In 1945, 41.9 workers contributed for every Social Security recipient. Today, as baby boomers enter retirement and birth rates decline, the worker-to-beneficiary ratio is 2.8.

According to the National Center for Health Statistics at the Centers for Disease Control and Prevention, births in the United States in 2017 were down 2% from 2016. It was the third straight year of decline, and it was the lowest number of births in 30 years (1987). There were approximately 60 births per 1,000 women ages 15-44, which is the lowest recorded rate since the government started tracking birth rates in 1909. The report said the number of births is now below the replacement rate which is the level at which a generation can exactly replace itself. The rate has generally been below replacement since 1971. And working longer may not be an option going forward. It may be a requirement. The government may increase the full retirement age beyond the current level of 67 in order to delay paying benefits and try to save the system.

Another traditional source of population growth in the U.S. has been immigration and both legal and illegal immigration is declining. The 2018 annual report of the Social Security trustees calculates that an increasing number of immigrants would help save the Social Security system, potentially keeping it solvent until 2092. On average, immigrants are younger than the overall U.S. population and have more years to work and pay into Social Security. The SSA’s estimates include legal immigrants, undocumented immigrants, and foreign workers on temporary visas.

Whether you’ll be able to retire is still the question. An ancient proverb says the wise person sees a problem and prepares. The fool goes blindly on. Now is the time to review your plans and see if you’re on the right path.Alhambra Investments can help you with your retirement planning. Call us today for a free consultation.

bob.williams@alhambrapartners.com 828-230-6690