The unemployment rate rose to 4.3 percent in July, and nonfarm payroll employment edged up

by 114,000, the U.S. Bureau of Labor Statistics reported today. Employment continued to trend

up in health care, in construction, and in transportation and warehousing, while information

lost jobs.

Household Survey Data

The unemployment rate rose by 0.2 percentage point to 4.3 percent in July, and the number of

unemployed people increased by 352,000 to 7.2 million. These measures are higher than a year

earlier, when the jobless rate was 3.5 percent, and the number of unemployed people was 5.9

million.

Among the major worker groups, the unemployment rates for adult men (4.0 percent) and Whites

(3.8 percent) increased in July. The jobless rates for adult women (3.8 percent), teenagers

(12.4 percent), Blacks (6.3 percent), Asians (3.7 percent), and Hispanics (5.3 percent) showed

little or no change over the month.

Among the unemployed, the number of people on temporary layoff increased by 249,000 to 1.1

million in July. The number of permanent job losers changed little at 1.7 million.

The number of long-term unemployed (those jobless for 27 weeks or more) changed little at 1.5

million in July. This measure is up from 1.2 million a year earlier. The long-term unemployed

accounted for 21.6 percent of all unemployed people in July.

Establishment Survey Data

Total nonfarm payroll employment edged up by 114,000 in July, below the average monthly gain

of 215,000 over the prior 12 months. In July, employment continued to trend up in health care,

in construction, and in transportation and warehousing, while information lost jobs. (See

table B-1.)

Health care added 55,000 jobs in July, similar to the average monthly gain of 63,000 over

the prior 12 months. In July, employment rose in home health care services (+22,000),

hospitals (+20,000), and nursing and residential care facilities (+9,000).

Employment continued to trend up in construction in July (+25,000), in line with the average

monthly gain over the prior 12 months (+19,000). Employment in specialty trade contractors

continued its upward trend in July (+19,000).

In July, employment continued to trend up in transportation and warehousing (+14,000), with

job gains in couriers and messengers (+11,000) and warehousing and storage (+11,000). These

gains were partially offset by a job loss in transit and ground passenger transportation

(-11,000). Transportation and warehousing has added 119,000 jobs since a recent low in January

of this year.

Employment in social assistance continued its upward trend in July (+9,000), but at a slower

pace than the average monthly gain over the prior 12 months (+23,000).

Information employment declined by 20,000 in July but has changed little over the year.

Government employment was little changed in July (+17,000). Employment growth in government

has slowed in recent months, following larger job gains in 2023 and the first quarter of 2024.

Commentary

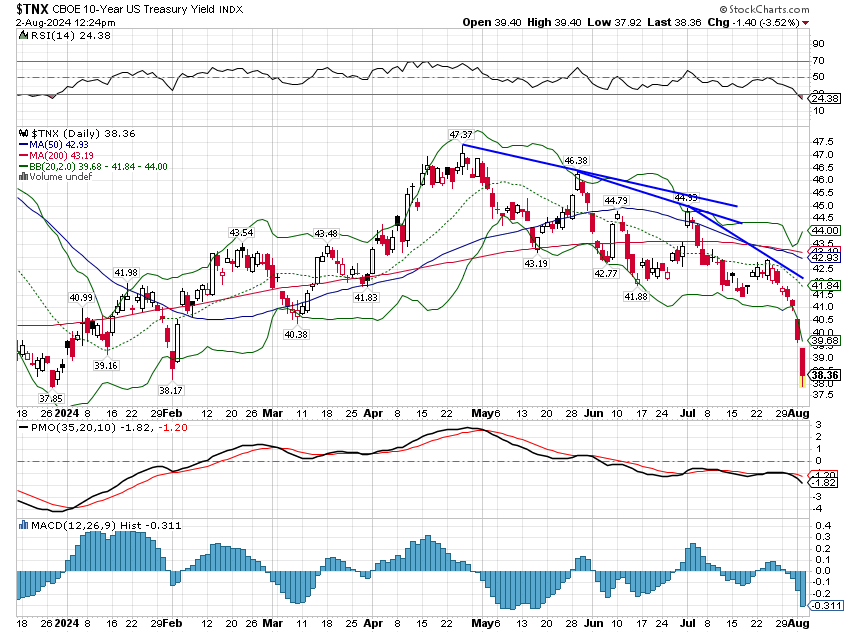

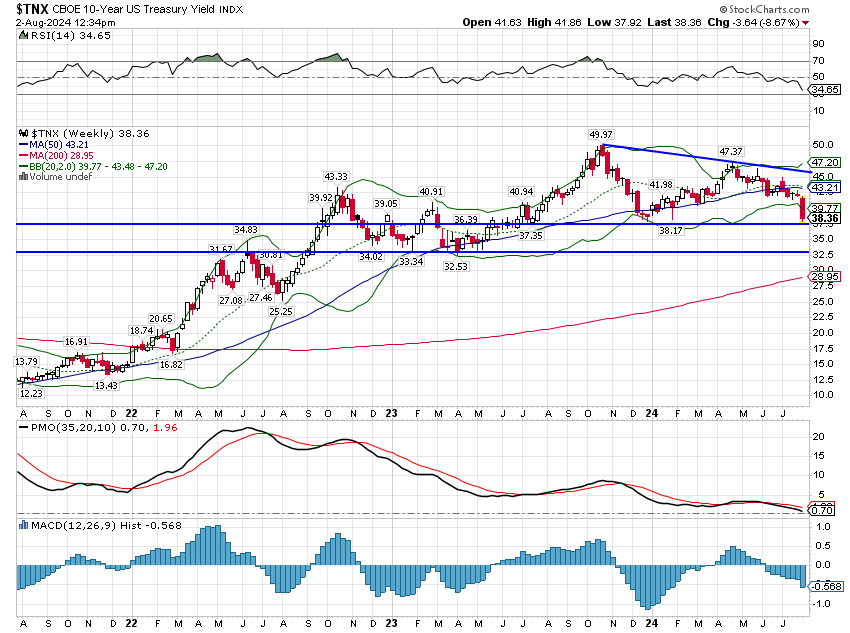

The employment report added to fears of a more significant economic slowdown that have been building for weeks. We can see this angst rising in the bond market where yields have fallen since peaking in late April. The 10 year Treasury yield has fallen roughly 90 basis points from its peak. As you can see the drop has accelerated over the last couple of weeks.

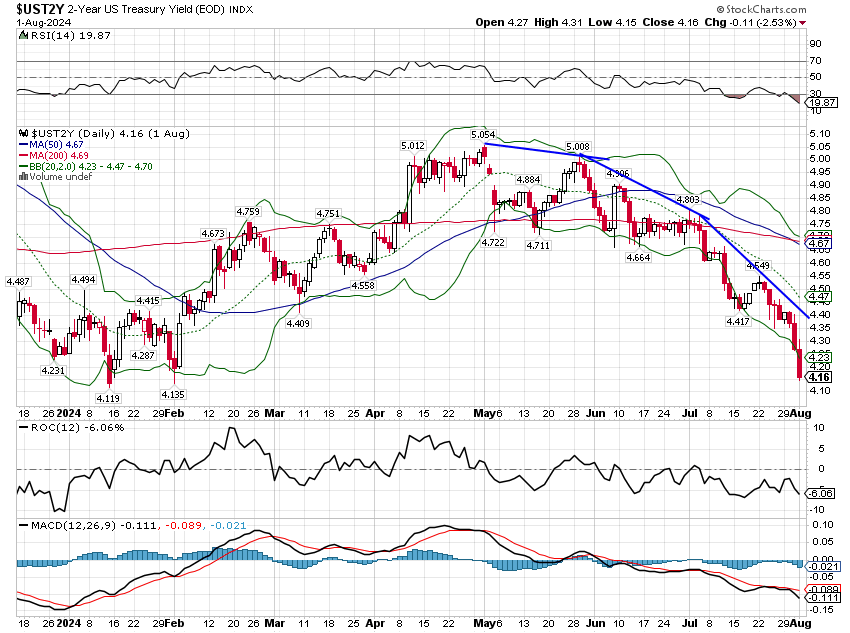

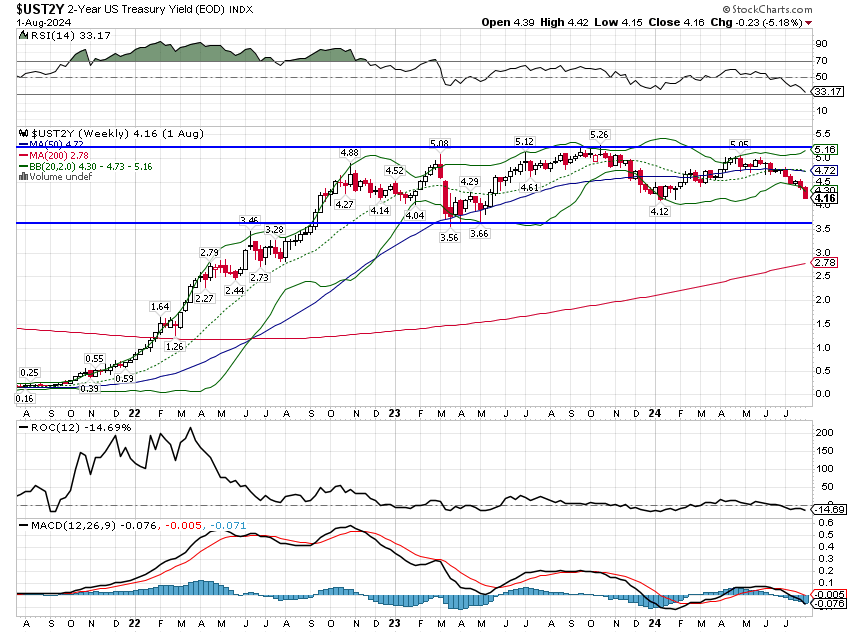

The 2 year Treasury yield has also fallen rapidly.

Falling yields are an indication that growth expectations have fallen from where they were at the peak. Long term investors should take a longer view though. Even after a big recent drop, rates are still in a range they’ve been in for nearly two years.

Employment reports are one of the most market moving economic releases on a monthly basis because the Fed has a dual mandate to steer the economy toward low inflation and to maintain growth. The Fed sees the unemployment rate as indicative of economic growth so rising unemployment is seen as increasing the likelihood the Fed will reduce interest rates. Hence, the movement in rates.

Unfortunately, the data produced on a monthly basis isn’t very accurate. The number of jobs created comes from the Establishment Survey of 119,000 businesses and government agencies representing approximately 629,000 work sites which is about 30% of the total. On a monthly basis it produces an estimate that is accurate to roughly + or – 100,000. The unemployment rate comes from a different survey called the Household Survey which calls on 60,000 households. Obviously, the accuracy of the survey leaves a lot to be desired.

There are some worrisome signs in the employment data but investors should remember that unemployment is a lagging indicator; companies lay people off after business slows not before. That is why the markets have reacted to negatively to two separate reports on the labor market this week.

The first is the weekly jobless claims data which showed a rise to 249,000. Rising new claims for unemployment benefits is obviously negative but, again, it has to be put into context. The current level of claims is rising but it is still well below the long term averages. Since 2000 weekly claims have averaged 377,000. Claims have rarely been below 300,000 since the 1970s (when there were a lot fewer workers). The only recession since the 1960s that started with claims below 300k was the 2020 COVID recession. So, while a rising trend is worrisome it is not at a level yet that should cause too much angst.

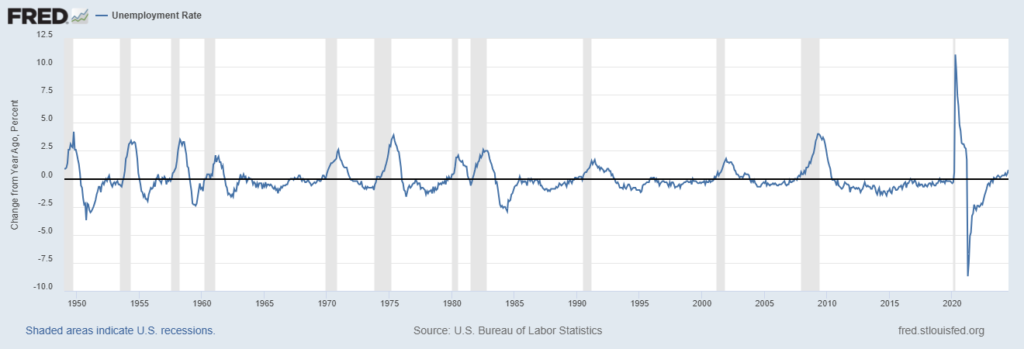

Second is the unemployment rate which has risen from a low 3.5% to 4.3% in July of this year. The year over year change has turned positive, which has, in the past, been a good indicator of recession:

I think this needs a caveat though. The unemployment rate rose primarily because, according to the Household Survey, the work force grew by 420,000 and the number of employed only rose 67,000. But that 420k number is way above the average since 2022 of 194k/month. Longer term, the average is even lower, about 100k per month dating back to the 1990s. So the unemployment rate may be rising but it’s probably being overstated.

The economy is still in the process of returning to “normal”, back to its pre-COVID trend of about 2% annual growth. There are some reasons to believe trend growth could increase in coming years – the impact of AI for instance – but we should wait for evidence of that before factoring it into our base case.

The number of jobs added in this report was below the 3 month average of 170,000 and well below the 3 month average a year ago of 242,000. So, yes the jobs market is slowing and has been slowing for a year. But it is still positive and there is nothing in this report that says recession is imminent and certainly nothing that should make you want to make big changes to your portfolio.

{kind=link}